|

#2

July 2nd, 2014, 03:15 PM

| |||

| |||

| Re: Question papers for CBSE 12th Commerce Accountancy

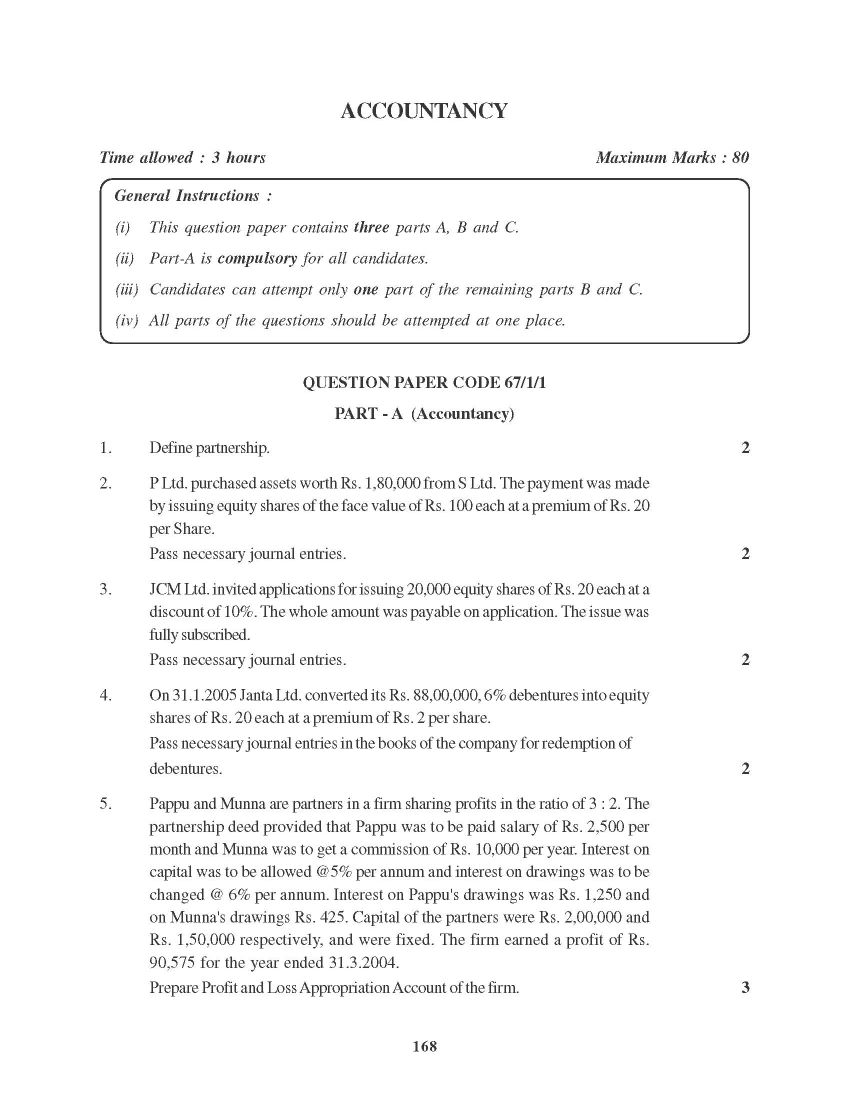

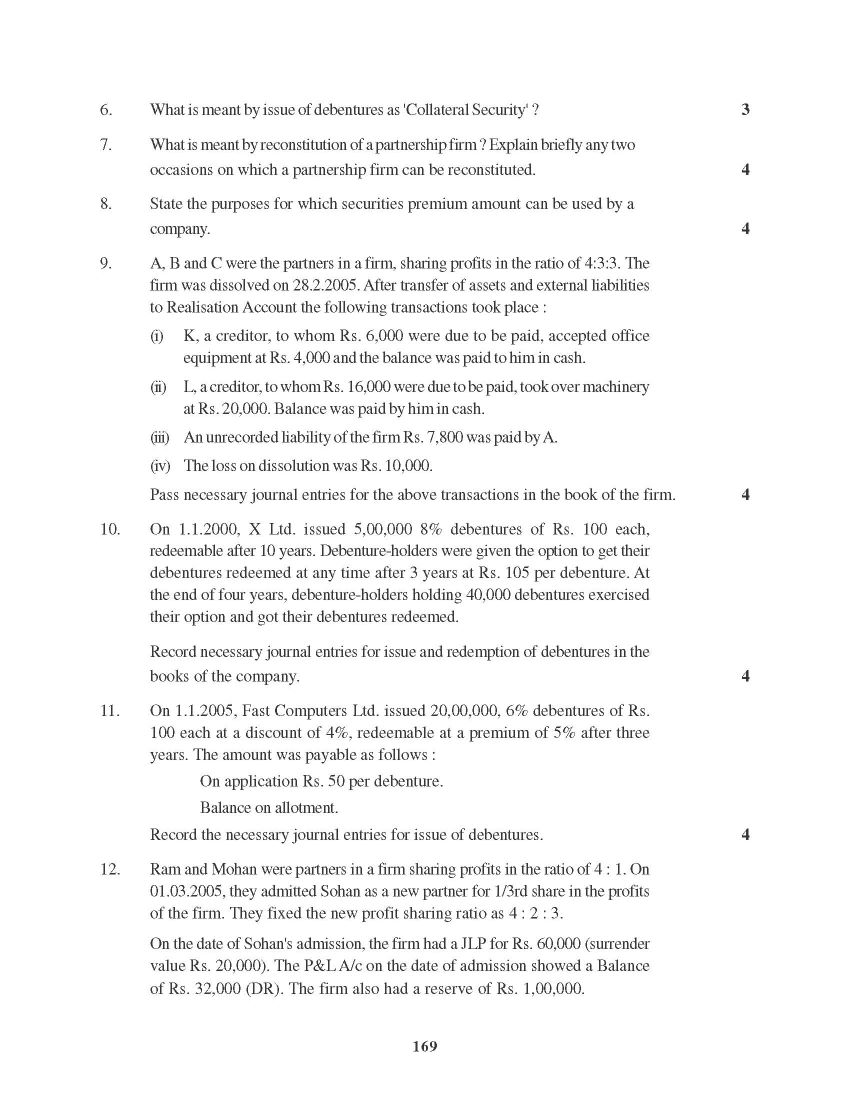

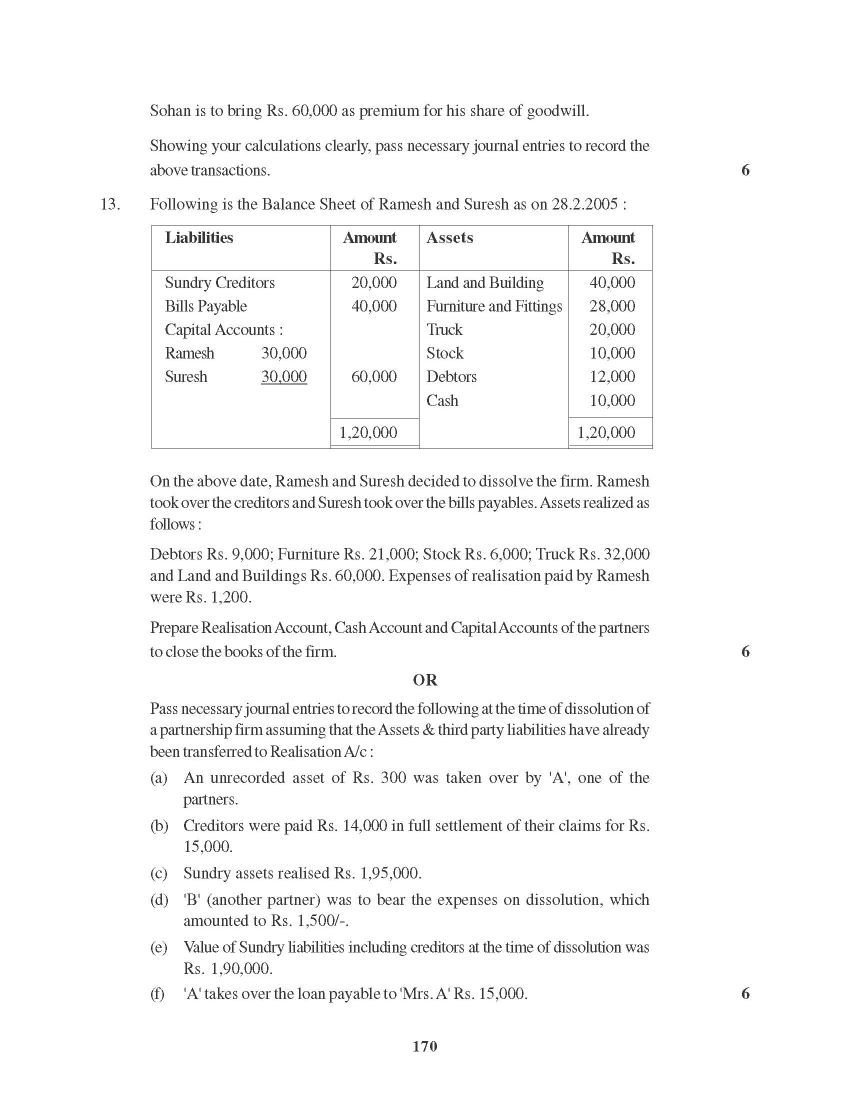

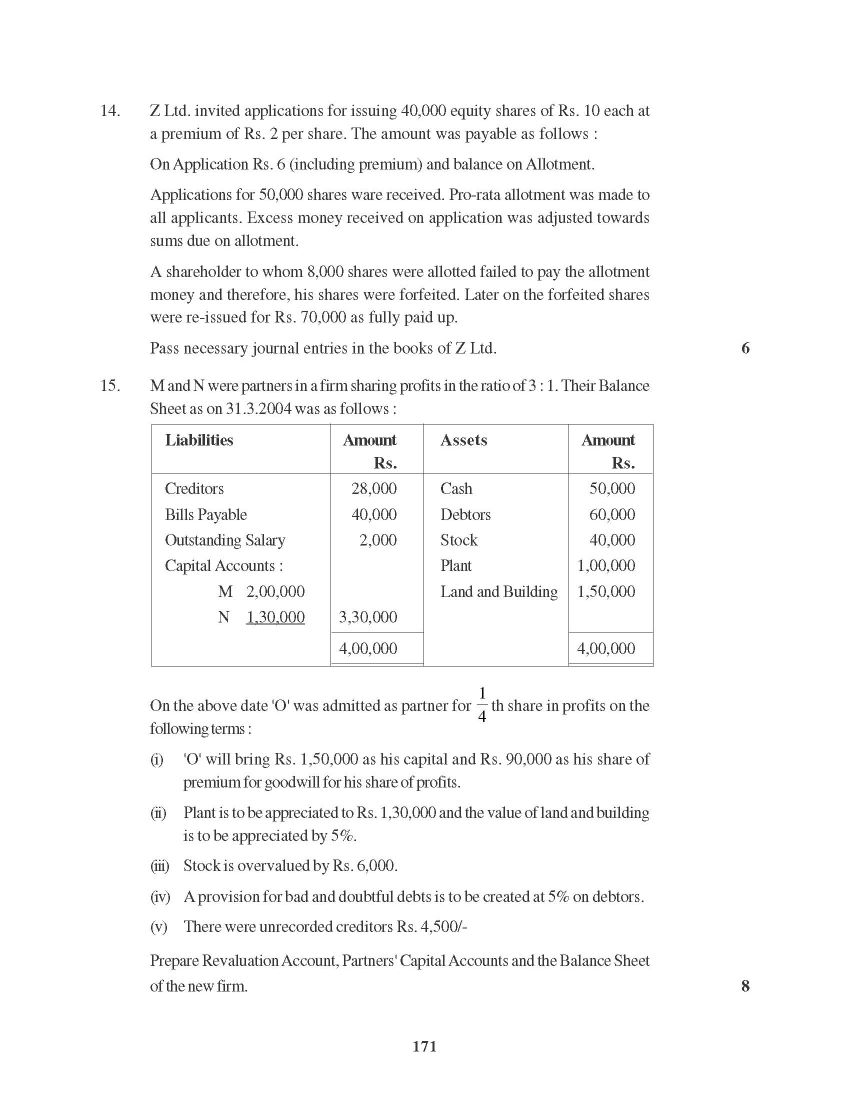

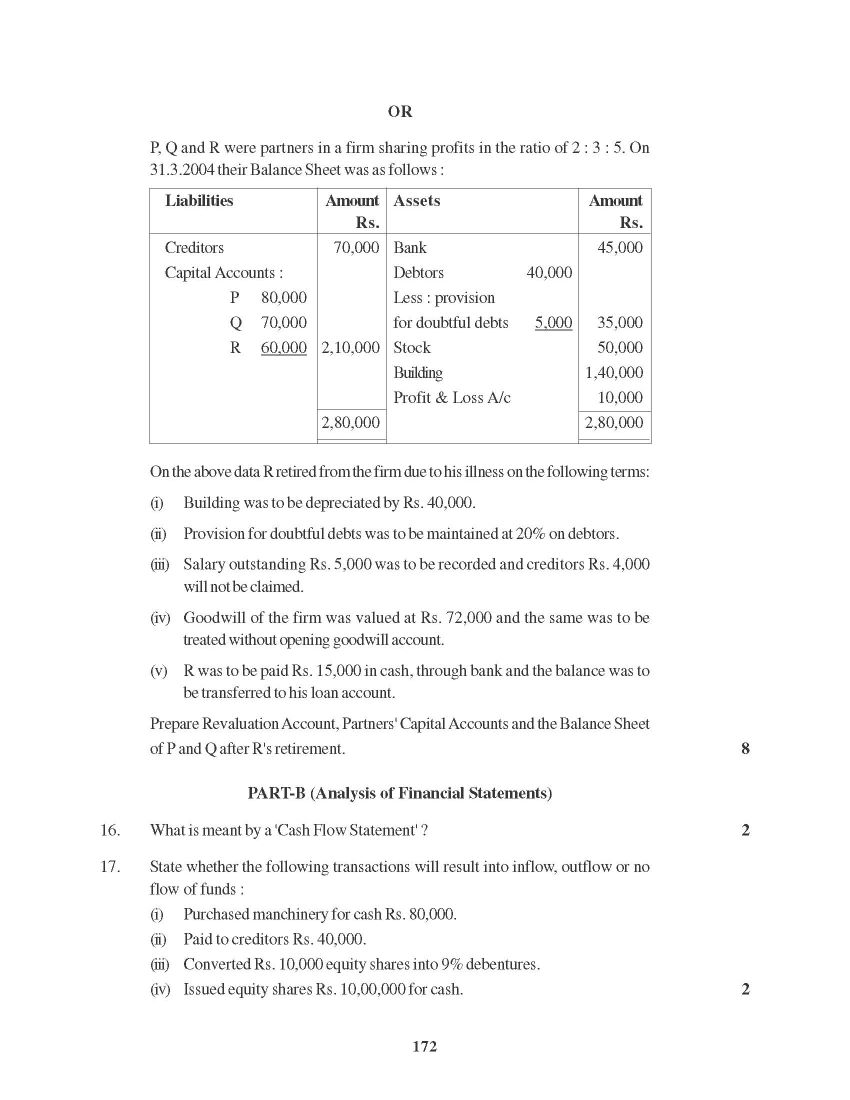

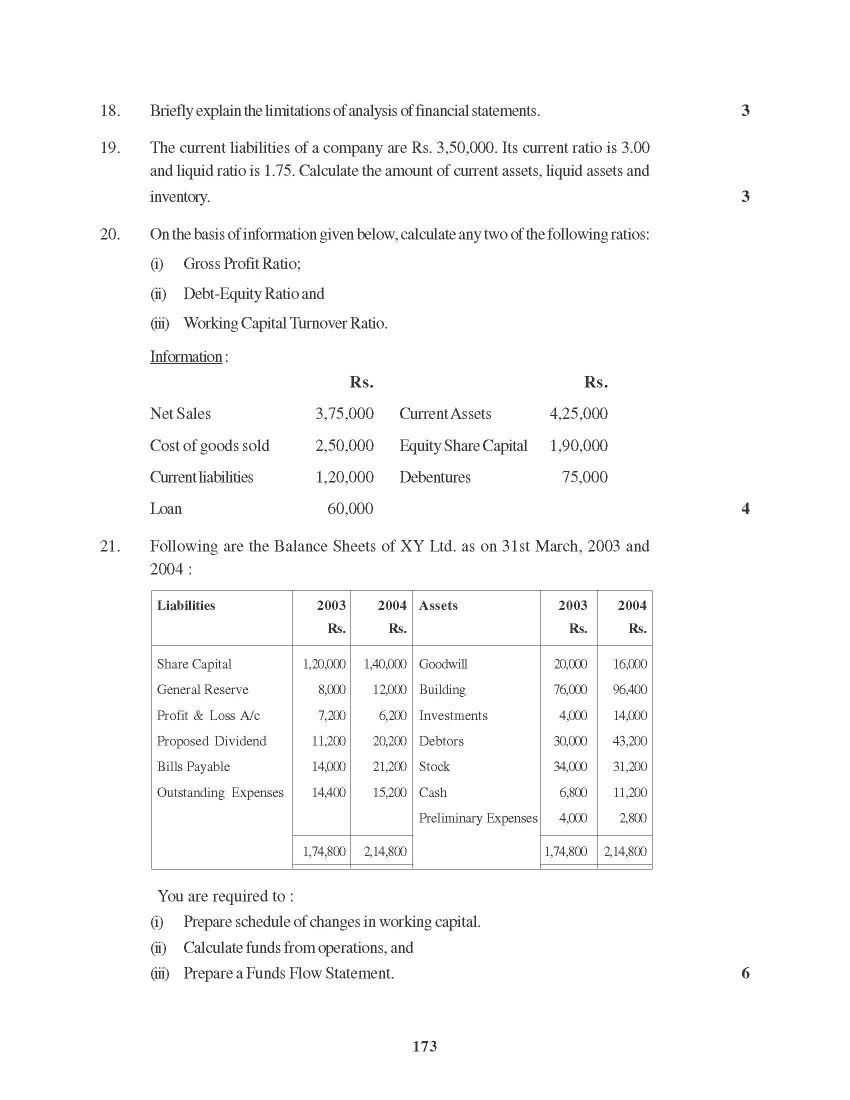

Here I am giving you question paper for CBSE 12th Commerce accountancy Question papers in PDF file attached with it so you can get it easily. 1. Define partnership. 2 2. P Ltd. purchased assets worth Rs. 1,80,000 from S Ltd. The payment was made by issuing equity shares of the face value of Rs. 100 each at a premium of Rs. 20 per Share. Pass necessary journal entries. 2 3. JCM Ltd. invited applications for issuing 20,000 equity shares of Rs. 20 each at a discount of 10%. The whole amount was payable on application. The issue was fully subscribed. Pass necessary journal entries. 2 4. On 31.1.2005 Janta Ltd. converted its Rs. 88,00,000, 6% debentures into equity shares of Rs. 20 each at a premium of Rs. 2 per share. Pass necessary journal entries in the books of the company for redemption of debentures. 2 5. Pappu and Munna are partners in a firm sharing profits in the ratio of 3 : 2. The partnership deed provided that Pappu was to be paid salary of Rs. 2,500 per month and Munna was to get a commission of Rs. 10,000 per year. Interest on capital was to be allowed @5% per annum and interest on drawings was to be changed @ 6% per annum. Interest on Pappu's drawings was Rs. 1,250 and on Munna's drawings Rs. 425. Capital of the partners were Rs. 2,00,000 and Rs. 1,50,000 respectively, and were fixed. The firm earned a profit of Rs. 90,575 for the year ended 31.3.2004. Prepare Profit and Loss Appropriation Account of the firm. 3 169 6. What is meant by issue of debentures as 'Collateral Security' ? 3 7. What is meant by reconstitution of a partnership firm ? Explain briefly any two occasions on which a partnership firm can be reconstituted. 4 8. State the purposes for which securities premium amount can be used by a company. 4 9. A, B and C were the partners in a firm, sharing profits in the ratio of 4:3:3. The firm was dissolved on 28.2.2005. After transfer of assets and external liabilities to Realisation Account the following transactions took place :       |